Medicare is not easy to get your hands around but you have to. The information below should help you learn about Medicare and be better prepared to make the appropriate choices and be better prepared when working with a Medicare professional.

Medicare

|

Medigap (Medicare Supplements)

|

|

You can sign up for Medicare beginning three months before you turn 65, and coverage can start as soon as the first day of your birthday month. The initial enrollment period lasts until three months after your 65th birthday.

If you fail to sign up during this seven-month window around your 65th birthday, you may be required to pay permanently higher premiums for late enrollment. |

There is a one-time Medigap open-enrollment period that starts the month you turn 65 and enroll in Part B and lasts six months. During this period, you have a guaranteed right to buy any Medigap policy sold in your state regardless of your health condition. After this period, you could be denied coverage or pay higher premiums. A Medigap policy gives some peace of mind that those expenses will be covered if you have very high medical expenses. These plans fill in many of Medicare's cost-sharing requirements and sometimes cover additional services that traditional Medicare doesn't cover.

|

Medicare.gov www.medicare.gov/basics/get-started-with-medicare

The standard Part B premium amount in 2022 is $170.10.

Part B deductible in 2022 is $233. After you meet your deductible for the year, you typically pay 20% of the Medicare-Approved Amount for these:

Part B deductible in 2022 is $233. After you meet your deductible for the year, you typically pay 20% of the Medicare-Approved Amount for these:

- Most doctor services (including most doctor services while you're a hospital inpatient)

- Outpatient therapy

- Durable Medical Equipment (Dme)

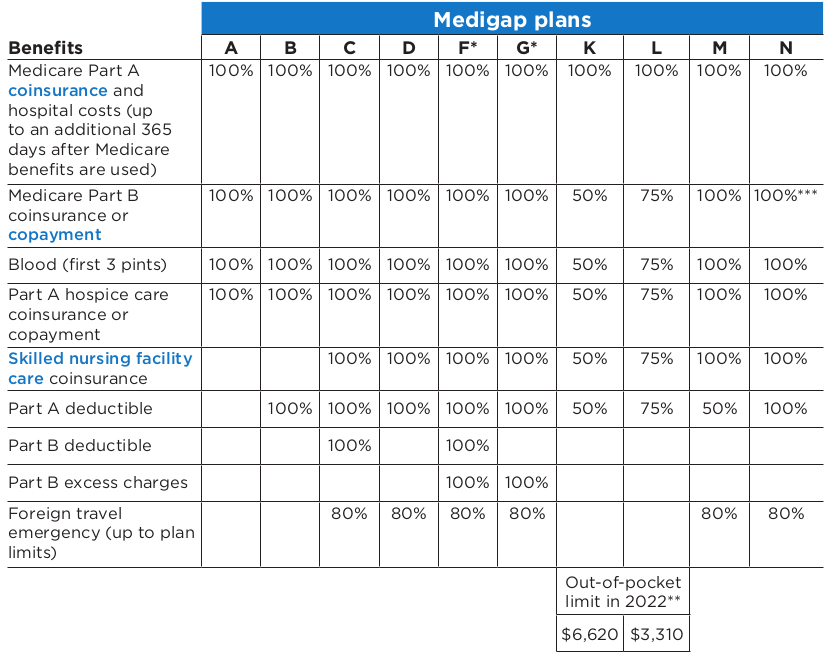

How do I compare Medigap plans?

The chart below shows basic information about the different benefits that Medicare Supplement Insurance (Medigap) plans cover for 2022. If a percentage appears, the Medigap plan covers that percentage of the benefit, and you’re responsible for the rest. Out-of-pocket costs (like deductibles) might change for 2023.

The chart below shows basic information about the different benefits that Medicare Supplement Insurance (Medigap) plans cover for 2022. If a percentage appears, the Medigap plan covers that percentage of the benefit, and you’re responsible for the rest. Out-of-pocket costs (like deductibles) might change for 2023.

* Plans F and G also offer a high-deductible plan in some states. With this option, you ust pay for Medicare-covered costs (coinsurance, copayments, and deductibles) up to the deductible amount of $2,490 in 2022 before your policy pays anything. (You can’t buy Plans C and F if you were new to Medicare on or after January 1, 2020. See previous page for more information.)

** For Plans K and L, after you meet your out-of-pocket yearly limit and your yearly Part B deductible ($233 in 2022), the Medigap plan pays 100% of covered services for the rest of the calendar year.

***Plan N pays 100% of the Part B coinsurance. You must pay a copayment of up to $20 for some office visits and up to a $50 copayment for emergency room visits that don’t result in an inpatient admission.

** For Plans K and L, after you meet your out-of-pocket yearly limit and your yearly Part B deductible ($233 in 2022), the Medigap plan pays 100% of covered services for the rest of the calendar year.

***Plan N pays 100% of the Part B coinsurance. You must pay a copayment of up to $20 for some office visits and up to a $50 copayment for emergency room visits that don’t result in an inpatient admission.

Fill The Holes In Your Medicare With The HMA™ Medical Benefits Account

⌂ Disclosure

I am licensed in Florida, New Jersey, Pennsylvania and Texas. If you live or if your company is based in any of these states, I can help you.

I am licensed in Florida, New Jersey, Pennsylvania and Texas. If you live or if your company is based in any of these states, I can help you.